After the lifting of the pandemic restrictions at the beginning of 2022, the Polish economy began on a path to dynamic growth. This positive trend was halted by Russia’s aggression against Ukraine in February. As a result of rising fuel and energy prices, persistent disruptions in supply chains and tightening of monetary policy, the pace of development of the Polish economy slowed from quarter to quarter. In 2022, the GDP was 4.9% higher than in the previous year, when it increased by 6.8%.

The weakening of the domestic economic situation last year was mainly due to household consumption. Despite the introduction of protective measures under the antiinflation shields, the high increase in prices had a negative impact on their purchasing power. As a result, in 2022 household spending increased by 3.0% compared to 6.3% in 2021.

Poland remains a European country with a significant level of inflation. By December 2022, prices were 16.6% higher than the year before. The Monetary Policy Council continued to tighten the monetary policy. Between January and September of that year, it raised interest rates eight times. The reference rate increased from 1.75% at the end of 2021 to 6.75% in September 2022. In the following months, the MPC maintained the interest rates. Minutes from the Council’s meetings indicated acceptance of the extended period of elevated inflation due to fears of an economic slowdown. As a result of the measures taken, the availability of loans was significantly reduced, both for enterprises and households (including by reducing the demand on the real estate market).

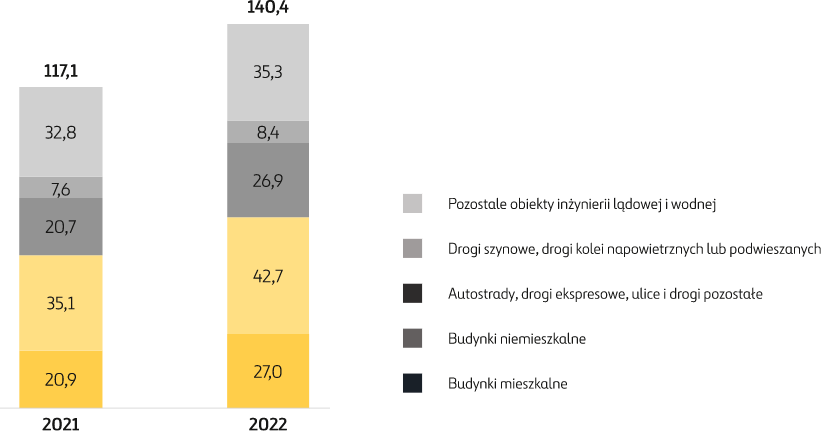

From the point of view of the construction sector, the dynamics of investments deserves special attention, which in 2022 was twice as high as in the previous year (4.5% vs. 2.1%). The value of construction and assembly production in current prices amounted to PLN 140.4 billion (an increase by 19.9% y/y). Production in the field of general construction (residential and non-residential buildings) reached the level of PLN 69.7 billion, 24.6% higher than in the previous year. A good economic situation occurred in both residential and non-residential construction, where the construction and assembly production increased by 29.4% and 21.8%, respectively.

In 2022, the value of infrastructural construction production amounted to PLN 70.6 billion, an increase by 15.5% compared to 2021 (including 29.9% in construction and assembly production for road construction and 10.2% in rail construction).

Despite Russia’s aggression against Ukraine and the increasing uncertainty on the international and domestic markets, the situation in the Polish construction sector has remained stable.

Construction and erection production in PLN billion

Source: GUS

In 2022, the positive trends in residential construction continued. 238,600 apartments, i.e. 1.7% more than in the previous year were handed over for use (when the increase was 6.3%). There was an increase in the number of premises handed over for use in both individual construction (by 3.2%) and intended for sale or rent (by 1.3%). In 2022, the number of building permits or notifications was lower than in the previous year. 297,400 of them were issued, which was 12.8% less than in 2021 (203,000 were intended for developers, which was a decrease by 4.9%).

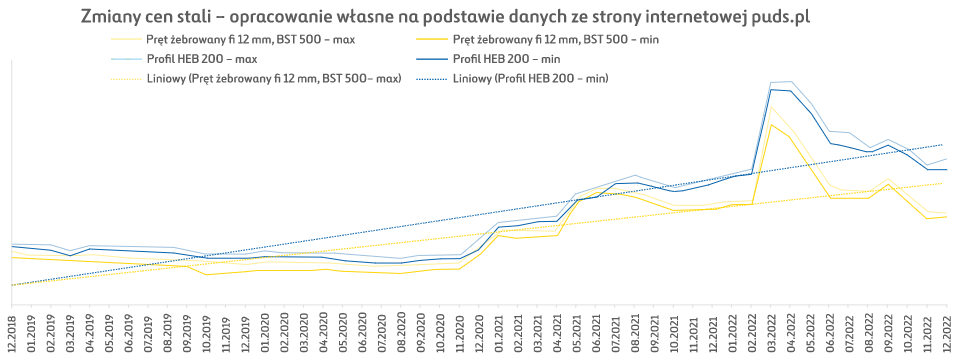

Lutowa agresja Rosji na Ukrainę spowodowała gwałtowny wzrost cen surowców na świecie. Przykładowo, po okresowym spadku cen stali, który miał miejsce na początku 2022 roku, jej ceny ponownie gwałtownie wzrosły po ataku Rosji na Ukrainę (do poziomu 1 375 euro za t w kwietniu). Pod koniec 2022 roku ceny stali wyraźnie spadały i wróciły do poziomów z końca 2021 roku. W grudniu 2022 roku kształtowały się na poziomie około 670 euro za 1 t. Podobny trend wystąpił także w przypadku innych materiałów i surowców budowlanych, co było spowodowane przede wszystkim spowolnieniem wzrostu gospodarczego i gorszymi prognozami rozwoju gospodarki światowej.

Changes in prices of steel bars

Changes in wholesale bitumen prices

Source: Indexation and price changes on the market – new data, GDDKiA (motorway agency), 9 January 2023

In order to limit the negative effects of the increase in the prices of building materials and wages on the profitability of projects, enterprises increased the prices of construction contracts. In 2022, the average prices of construction and assembly production were 12.6% higher than in the previous year.2

Being aware of the situation in the industry, in February 2022 the Ministry of Infrastructure introduced a change in the indexation system for road contracts, increasing the indexation limit from 5% to 10%. It applies to tenders announced in 2022 for tasks carried out under the Design and Build system. Equal risk sharing between project owners and contractors remained unchanged. In the period from July to December 2022, GDDKiA signed indexation annexes for 115 projects carried out by 26 contractors. The annexes signed relate to ongoing projects as part of the government programmes for the Construction of National Roads for 2014–2023 (with a perspective until 2025) and Construction of 100 Bypasses for 2020–2030. The annexes include remuneration for work performed after 24 February 2022, i.e. after Russia’s aggression against Ukraine and the related economic consequences.

In 2022, the average employment in the construction industry was 432,000 people, 2.2% higher than in 2021. In December last year, a construction worker received an average of PLN 7,022 from their salary compared to PLN 6,360 the year before, which means an increase by 10.4%. This was primarily the effect of wage pressure conditioned by rapidly growing inflation.

According to Coface, 280 insolvent construction companies were registered by the end of 2022, i.e. 37% more than a year before. These were mainly small entities. The increase in the number of insolvent enterprises resulted from a combination of many factors – both of a supply and demand nature. The high prices of building materials, which started to fall at the end of the year, were still higher than in 2021. Growing salaries and the outflow of employees due to the mobilisation of men in Ukraine have also become a challenge for the sector.

According to the forecasts of the Polish Economic Institute (PIE), published in December 2022, in 2023 Poland and other economies in the European Union will face a slowdown. According to analysts, the domestic economy is heading towards a shallow recession. Throughout 2023, GDP is likely to increase by 1.2%, while experts expect a recession at the beginning of the year (GDP decline in the first quarter by 0.3% y/y). In the second half of the year, an increase in economic activity is expected due to the improvement in the economic situation in the euro area. Poland will struggle with increased inflation which, according to analysts, should slow down in 2024. In 2023, CPI inflation is expected to be 13%, compared to 14.4% in 2022.

The GDP growth forecast published in March 2023 by NBP assumes that in 2023 it will increase by 0.9%. The Polish economy should still be under the influence of strong negative shocks, including the raw material shocks, strengthened by the effects of Russia’s aggression against Ukraine. Economic activity in Poland will also be adversely affected by a marked slowdown in the rate of economic growth abroad, as well as the gradually materialising effects of the previous NBP interest rate increases. At the same time the scale of the deterioration in the domestic economic situation should be mitigated by a number of protective measures for households and sensitive entities related to the increase in prices of energy carriers. Household spending, which in recent years has been the main driver behind GDP growth, in 2023 is likely to increase by only 0.9%. It will be limited by: high inflation predicted in the coming quarters, reducing the purchasing power of the population, depressed moods, and the effects of the previous NBP interest rate increases. The impact of these factors will be partially counteracted by the legislative solutions introduced by the government in the field of energy policy.

The economic situation in Poland in 2023 will be largely determined by the course of Russia’s aggression against Ukraine.

In 2023, the investment climate in Poland will be influenced by the armed conflict taking place beyond the Polish border. Investment demand will be adversely affected by the still high prices of raw materials in the global markets and higher costs of energy consumption and project execution, as well as a decrease in investment optimism resulting from concerns about lower demand on both the domestic and foreign markets. The volume of private investment outlays, including housing demand in particular, will be adversely affected by the spread-over-time effects of the previous increases in NBP interest rates, limiting the availability and increasing the cost of credit. Under the influence of the above factors, gross fixed asset expenditures in 2023 will probably be at the level of 2022.

The size of public projects largely depends on the level of absorption of EU funds. The NBP has assumed that they will grow, while the implementation of already started projects under the KPO (National Reconstruction Plan) will be temporarily financed from national funds.

The key challenge in 2023 will be the persistently high level of inflation. According to NBP, in 2023 the average inflation will be at the level of 11.9%.

Future economic activity and the path of inflation in Poland will largely depend on the scale of disturbances in the functioning of the global economy caused by Russia’s military aggression against Ukraine. An important source of risk for economic conditions abroad is also the future shape of the monetary policy of major central banks.

Poland was the largest beneficiary of EU funds in the 2014–2020 perspective (co-financing value of EUR 86.1 billion). By the end of 2022, agreements for co-financing projects had been signed, with the total value of subsidies amounting to PLN 349.1 billion, i.e. 99.1% of the entire available allocation of EU funds. On the other hand, the value of total expenditures of beneficiaries settled at the national level amounted to PLN 424.5 billion, including PLN 274.0 billion of EU co-financing, which constitutes 77.8% of the allocation.

In December 2021, the Polish government submitted the Partnership Agreement to the European Commission regarding the allocation of EU funds under the next financial perspective of the European Union for 2021–2027. The proposed value of the funds allocated to Poland is EUR 76 billion in current prices, compared to EUR 82.5 billion in current prices which were allocated to Poland under the previous financial perspective. EUR 24.2 billion from EU funds has been allocated to the Infrastructure and Environment (FEnIKS) programme, compared to EUR 27.4 billion in the previous financial perspective. Despite the decrease in the value of allocations, Poland still remains the largest beneficiary of EU funds. The expected scale of support in the area of infrastructural projects should allow the maintaining of the significant role of these funds in the development of the Polish construction sector in the coming years. The forthcoming budget perspective will be the first to prioritise rail investment over road investment. It will also be important in supporting infrastructural projects under the Connecting Europe Facility (CEF) competition instrument. An additional source of investment financing could be the Reconstruction Fund. As part of the subsidies, Poland should receive PLN 23.9 billion, including PLN 12 billion for railways 3) Source: Ministry of Funds and Regional Policy and PLN 3.2 billion for roads under transport projects. In addition, we can apply for PLN 34.2 billion in loans. As a result of the low pace in implementing milestones, the government decided to pre-finance projects through the Polish Development Fund. The estimated level of support in 2023 under the instrument is PLN 15 billion.

An important investment project in Poland, which construction companies count on, is the Central Communication Port (CPK) Project – the construction of the Solidarity port. This is in the first stage of works which should last until 2023 and cost PLN 13 billion. In the airport part, the planning phase has been completed. The design stage is currently underway. A contract was signed with the designer of the passenger terminal and the railway station (master architect) – a consortium consisting of Foster + Partners and Buro Happold, and with the Master Civil Engineer (MCE) – the Lebanese Dar Al-Handasah group of companies which was involved in the design of airports, including in Doha, Dubai and Chicago. In addition, 13 companies and consortia have been selected with which the CPK will sign a framework agreement as part of the first tender for the design of supporting facilities (SIE – Support Infrastructure Engineer). Bids submitted in the second part of the tender announced in October, known as SIE2, for the airport (including hotels, offices, multi-storey car parks, commercial facilities and cargo terminals) are still being analysed.