4.2. Alignment with the European Union Taxonomy, Environmental responsibility

4.2. Alignment with the European Union Taxonomy

What is the EU Taxonomy?

The EU Taxonomy is a classification system that establishes criteria that economic activities must meet to be considered environmentally sustainable. It is a set of pan-European principles and technical indicators that reflect the EU’s climate goals and ambitions for specific areas of the economy, and is designed to redirect capital flows toward more sustainable activities to implement the EU climate and broader environmental policies over the 2030 horizon and beyond. The Taxonomy provides companies, investors and policymakers with clear and uniform definitions of environmentally sustainable activities. In this way, it helps protect companies and investors from greenwashing. among other things.

An environmentally sustainable economic activity is one that meets the following criteria:

- contributes substantially to one or more environmental objectives,

- does not significantly harm any of the environmental objectives,

- is carried out in accordance with minimum safeguards,

- complies with technical screening criteria.

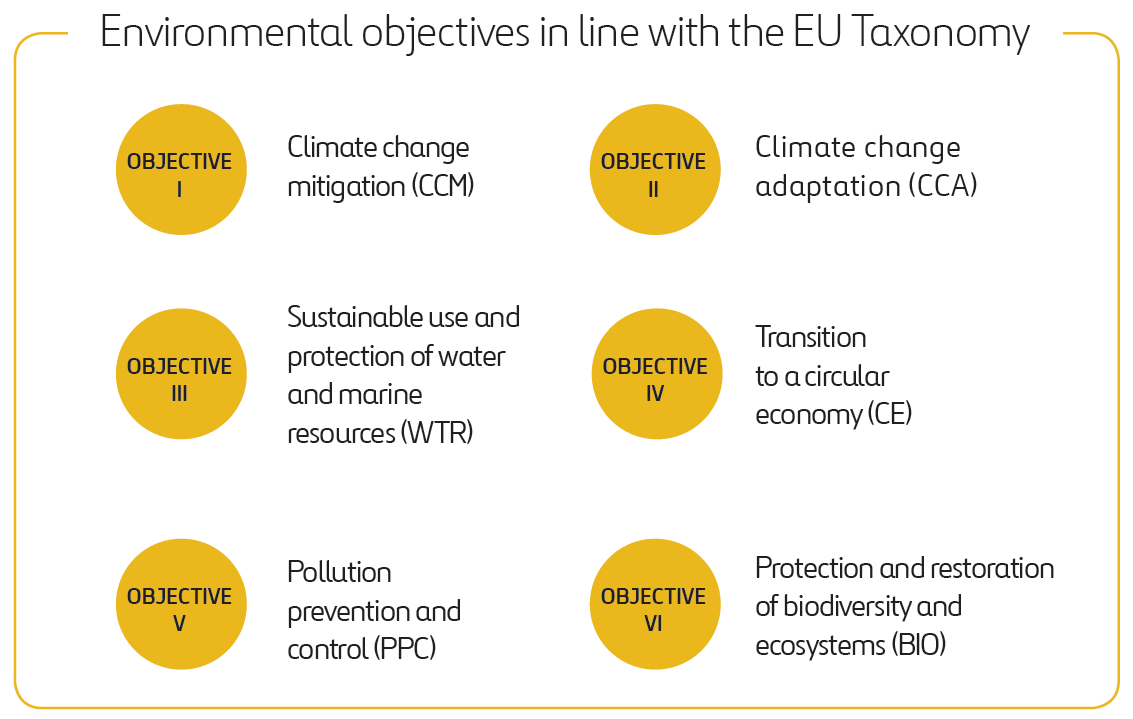

Environmental objectives aligned with the taxonomy include:

- climate change mitigation,

- climate change adaptation,

- sustainable use and protection of water and marine resources,

- transition to a circular economy,

- pollution prevention and control,

- protection and restoration of biodiversity and ecosystems.

In accordance with the Taxonomy Regulation [1], in the non-financial report the Group discloses:

- the percentage of revenue derived from products or services related to environmentally sustainable activities,

- the percentage of capital expenditures (CAPEX) corresponding to assets or processes related to environmentally sustainable activities,

- the percentage of operating expenses (OPEX) corresponding to assets or processes related to environmentally sustainable activities.

Detailed requirements for the calculation and disclosure of the aforementioned indicators are set forth in Commission Delegated Regulation (EU) 2021/2178 [2]), the so-called Article 8 Delegated Act.

Budimex Group’s Taxonomy alignment examination process

A four-step process was conducted to verify alignment with the taxonomy:

1. Identification

The stage consisted of reviewing all the activities carried out by the Budimex Group and determining which activities are EU Taxonomy-eligible. The review covered the companies’ earned revenues, capital expenditures and operating expenses. To identify individual activities the companies used the descriptions in the annexes to Commission Delegated Regulation (EU) 2021/2139, as amended (i.e. supplemented by Commission Delegated Regulation (EU) 2023/2485) and Commission Delegated Regulation (EU) 2023/2486. In case of insufficient clarity in the qualification of the activities, the NACE code classification was used as an auxiliary measure [3].

Eligibility was assessed against all six environmental objectives for which lists of eligible activities were published:

OBJECTIVE I – Climate change mitigation (CCM) – as per Annex I of Commission Delegated Regulation (EU) 2021/2139 and for new activities added to the catalog of activities supporting Objective I as defined in Commission Delegated Regulation (EU) 2023/2485

OBJECTIVE II – Climate change adaptation (CCA) – as per Annex II of Commission Delegated Regulation (EU) 2021/2139 and for new activities added to the catalog of activities supporting Objective II as defined in Commission Delegated Regulation (EU) 2023/2485

For the other four environmental objectives set forth in the corresponding annexes to Commission Delegated Regulation (EU) 2023/2486:

OBJECTIVE III – Sustainable use and protection of water and marine resources (WTR),

OBJECTIVE IV – Transition to a circular economy (CE),

OBJECTIVE V – Pollution prevention and control (PPC),

OBJECTIVE VI – Protection and restoration of biodiversity and ecosystems (BIO).

The Group has identified activities eligible for the first two environmental objectives in the previous and current reporting periods. For the current reporting period, the Group has confirmed that the economic activities that concern the Group and are eligible for the other four environmental objectives overlap with the economic activities already identified as eligible for the first two environmental objectives.

2. Allocation

The allocation stage consisted of assigning the value of revenue, capital expenditures and operating expenses to the various identified activities eligible for the EU Taxonomy. Details of the allocation methods used are described in the “Accounting principles” section.

3. Verification of alignment

The stages of verification of alignment with the EU Taxonomy consisted of two levels of evaluation, as described below:

- For activities pertaining to the first two environmental objectives (OBJECTIVE I and OBJECTIVE II), an assessment of the criteria of substantial contribution and doing no significant harm was carried out using the technical eligibility criteria set out in the annexes to Commission Delegated Regulation (EU) 2021/2139. Details of the assessment are presented in the section “Verification of alignment with technical eligibility criteria.”

- The fulfillment of minimum safeguards was based on the evaluation conducted in 2022 and the recommendations implemented in 2023. Details of the assessment conducted are presented in the “Minimum safeguards” section.

In accordance with Commission Delegated Regulation (EU) 2021/2178 (as amended by Commission Delegated Regulation (EU) 2023/2486). the Budimex Group will assess eligibility and alignment for the remaining activities (i.e. for new activities under the first two objectives and for activities under the remaining four environmental objectives) starting from the disclosures published for 2024.

4. Calculation

The process consisted of using the results of verification from stages two and three to produce tables containing the required data in accordance with the requirements of Annexes I and II to Commission Delegated Regulation (EU) 2021/2178, as amended.

The verification was carried out by representatives of the ESG, Quality and Environmental Protection Department [4], representatives of the Controlling Department and contract representatives of Group companies.

Verification of alignment with technical eligibility criteria

Verification of alignment with technical eligibility criteria was carried out for all taxonomy-eligible activities, and consisted of analyzing the individual criteria of substantial contribution and not causing significant harm in relation to OBJECTIVE I and OBJECTIVE II, and verification of the extent to which the type of activity complies with the technical eligibility criteria set forth in Annexes I and II to Commission Delegated Regulation (EU) 2021/2139 [5], as extended by Commission Delegated Regulation (EU) 2022/1214 [6]. The Group carried out the taxonomy assessment on the basis of active contracts, which are in the implementation phase (in the case of Budimex SA. the analysis was carried out on projects that were operational; no technical eligibility criteria were analyzed for contracts in the design phase). During the process of verifying the technical eligibility criteria for activities found not to meet the criterion of substantial contribution, no analysis of the criteria for not causing significant harm was carried out.

The main types of activities carried out in the Group are those included in the taxonomy as 6.14 Infrastructure for rail transport, 6.16 Infrastructure enabling low carbon water transport, 7.1 Construction of new buildings, 7.2 Renovation of existing buildings, 5.5 Collection and transport of non-hazardous waste in source segregated fractions and 5.9 Material recovery from non-hazardous waste.

The analysis of alignment with the technical eligibility criteria was carried out from October 2023 to December 2023 by representatives of Budimex SA’s ESG, Quality and Environmental Protection Department [7] as part of the work specified in the contracts for services provided by the Group to its business partners. The verification used tools in the form of alignment checklists implemented from the Ferrovial Group, which is the majority investor in the Budimex Group. In particular, documents such as environmental impact assessments, environmental monitoring plans, construction and demolition waste recovery rate reports, flora and fauna management plans, and corrective action plans for mitigating noise, dust, among others, were analyzed to assess whether DNSH criteria are met.

The analysis was conducted on the basis of active contracts generating revenue in 2023 or on the basis of active contracts or assets held by the Group that generate capital expenditures or operating expenses. In this way, the percentage of revenue, capital expenditures and operating expenses aligned with the technical eligibility criteria, which are reported in the tables in this section of the non-financial report, was established for each of the activities.

Verification of alignment with minimum safeguards

According to Article 18 of Regulation 2020/852:

The minimum safeguards referred to in point (c) of Article 3 shall be procedures implemented by an undertaking that is carrying out an economic activity to ensure the alignment with the OECD Guidelines [8] for Multinational Enterprises and the UN Guiding Principles on Business and Human Rights, including the principles and rights set out in the eight fundamental conventions identified in the Declaration of the International Labour Organisation on Fundamental Principles and Rights at Work and the International Bill of Human Rights.

The alignment with the minimum safeguards was based on the assessment conducted in 2022 and the recommendations implemented in 2023. The examination of compliance with the minimum safeguards was conducted in accordance with the recommendations in the Final Report on Minimum Safeguards by the Platform on Sustainable Finance.

According to the recommendations, the following four signs point to non-compliance with the minimum safeguards:

- inadequate or non-existent corporate due diligence processes on human rights. including labor rights, bribery, taxation, and fair competition,

- the company has been held finally liable or found to have breached labor or human rights laws in certain types of labor or human rights court cases,

- the lack of collaboration with the OECD National Contact Point (hereafter OECD NCP) on a notification accepted by the OECD NCP,

- Business and Human Rights Resource Centre (BHRRC) made the allegation against the company, and the company did not respond within 3 months.

In the Budimex Group’s verification process, non-compliance based on the above-mentioned signs was examined as follows,

- Sign 1: The verification of the completeness of due diligence processes was based on internal verification of the existence and operation of due diligence process elements derived from the framework of those processes contained in the documents listed in the definition of minimum safeguards. The design of due diligence processes as defined proposed in Article 3(c) of Regulation (EU) 2020/852 of the European Parliament and of the Council of 18 June 2020 on the establishment of a framework to facilitate sustainable investment, and amending Regulation (EU) 2019/2088 is primarily influenced by the provisions of the UN Guiding Principles on Business and Human Rights and the OECD Guidelines for Multinational Enterprises. The verification of compliance was carried out with a compliance assessment tool using the assessment methodology proposed by the Platform on Sustainable Finance: World Benchmark Alliance Core UNGP [9] As a result of the analysis, it was determined that the organization has in place a functioning complete due diligence process that fulfills the guidelines.

- Sign 2: This sign was verified in the process of supplementing the responses to Sign 1 by verifying that there were no final convictions against the persons listed in the body of the sign during the period under review. As a result of the verification, it was found that there was no information qualifying the Group to meet the conditions of sign 2.

- Sign 3: A verification of the OECD NCP notification database [10] was conducted, showing that no notifications occurred against the Group during the period under review.

- Sign 4: A verification of the BHRRC notification database [11] was conducted, showing that no notifications occurred against the Group during the period under review.

As a result of the verification process, it was determined that the Group’s activities are carried out in compliance with the minimum safeguards.

Accounting principles

The following rules were used to calculate the percentage of revenue, capital expenditures (CAPEX) and operating expenses (OPEX) that are taxonomy-eligible or aligned:

Revenue

The denominator of the taxonomy’s revenue-related indicators is the Budimex Group’s total consolidated revenue in 2023, as disclosed in the consolidated financial statements in the consolidated profit and loss account under “Revenue from contracts with customers.” Revenues from sales of products, goods and materials are described in Note 30.

The numerator of the EU taxonomy-eligible revenue indicator included revenues from taxonomy-eligible activities (aligned and non-aligned). The numerator of the EU taxonomy-aligned revenue indicator included the portion of revenues that result from activities aligned with the technical criteria.

Capital expenditures (CAPEX)

The denominator of the taxonomy indicators for capital expenditures (CAPEX) is the capital expenditures incurred at all Group companies. which are reported in the consolidated statement of cash flows in investing activities under “Acquisition of intangible assets and property, plant and equipment.”

The numerator of the indicator of EU Taxonomy-eligible expenditures includes the portion of CAPEX that relates to the types of activities eligible for the taxonomy (aligned and non-aligned with technical criteria). The numerator of the EU Taxonomy-aligned expenditure indicator includes the portion of CAPEX that relates to activities that are aligned with technical criteria.

The main capital expenditures in the year under review pertained to Budimex SA and FBSerwis Group companies. For capital expenditures incurred for vehicles, equipment, machinery, expansion of handling bases and storage facilities, the direct allocation method was applied to the type of activity in which the acquired assets will be used. For the remaining expenditures not directly mappable to taxonomic activity types, a proportional allocation method was used, as they will be used in the performance of various contracts, both related to taxonomy-eligible and non-eligible activities.

Operating expenses (OPEX)

The denominator of taxonomy indicators for operating expenses (OPEX) represents (as required by Annex I to Commission Delegated Regulation (EU) 2021/2178) all direct, non-capitalized costs that relate to research and development, building renovation measures, short-term lease, maintenance and repair, and any other direct expenditures relating to the day-to-day servicing of the Group’s assets of property, plant and equipment that are necessary to keep such assets in good condition.

The numerator of the indicator of EU Taxonomy-eligible expenses includes the portion of OPEX that relates to the types of activities eligible for the taxonomy (aligned and non-aligned with technical criteria). The numerator of the EU Taxonomy-aligned expense indicator includes the portion of OPEX that relates to activities that are aligned with technical criteria.

In the case of operating expenses for construction machinery and equipment, the direct allocation method was applied in a manner analogous to the CAPEX case described above. For other operating expenditures not directly attributable to activity types, the indirect allocation method was used.

Other information

The data used for the calculations came from the Budimex Group’s financial and accounting system and from the financial and accounting systems of the individual subsidiaries comprising the Group.

The Group avoided double counting when allocating revenue and capital expenditures by making appropriate consolidation exclusions, in accordance with applicable accounting regulations. For operating expenses, which are defined in the Commission’s Delegated Regulation (EU) 2021/2178 in a manner that does not refer to international financial reporting standards, all accounts in the Group’s accounting system were reviewed, and then the identified items meeting the definition of OPEX were assigned to given the taxonomy-eligible activity type in each case.

The Group discloses in this report for the second time the share of taxonomy-aligned activities and for the third time the share of activities that are taxonomy-eligible. The disclosure in this report relates to the most recent financial year, i.e. the period 1 January – 31 December 2023.

The analysis showed that there was no need for a detailed disaggregation of key performance indicators among the Group’s operating units in accordance with Section 1.2.2.3. Annex I to Commission Delegated Regulation (EU) 2021/2178. For more information, see the comments on each key performance indicator.

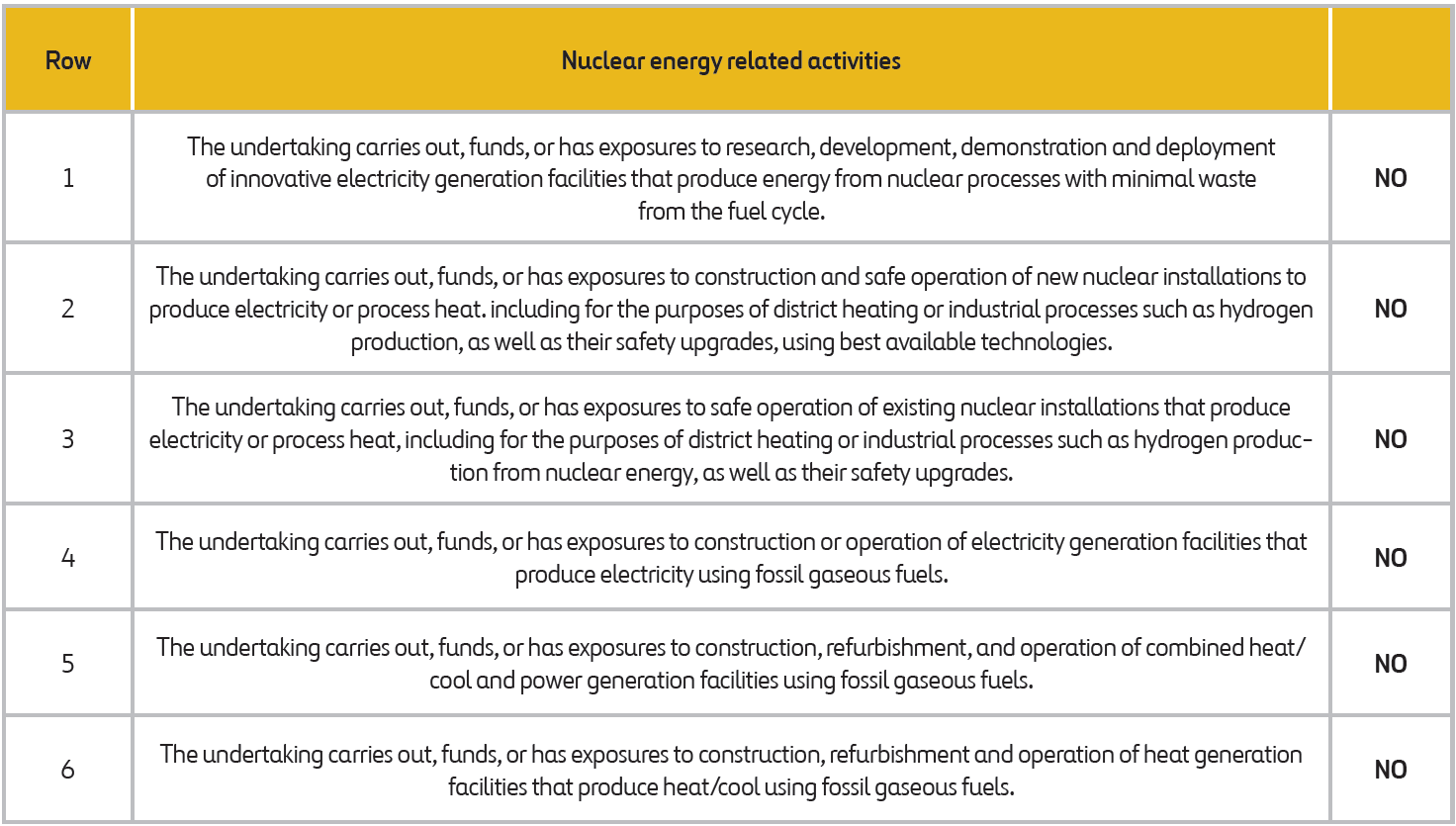

The Group does not carry out, finance or have exposure to the activities referred to in Sections 4.26-4.31 of Annexes I and II to Commission Delegated Regulation (EU) 2021/2139 (activities related to nuclear power generation and energy production from gaseous fossil fuels). Accordingly, the Group only discloses the following qualitative regulatory formula in this regard and does not disclose the other quantitative tables set forth in Annex XII of Commission Delegated Regulation (EU) 2021/2178, when all of these quantitative tables would contain zero values for activities related to fossil gas or nuclear energy.

Table: Nuclear energy related activities

Detailed results of the analysis are provided in tables: Revenue, CAPEX, and OPEX.

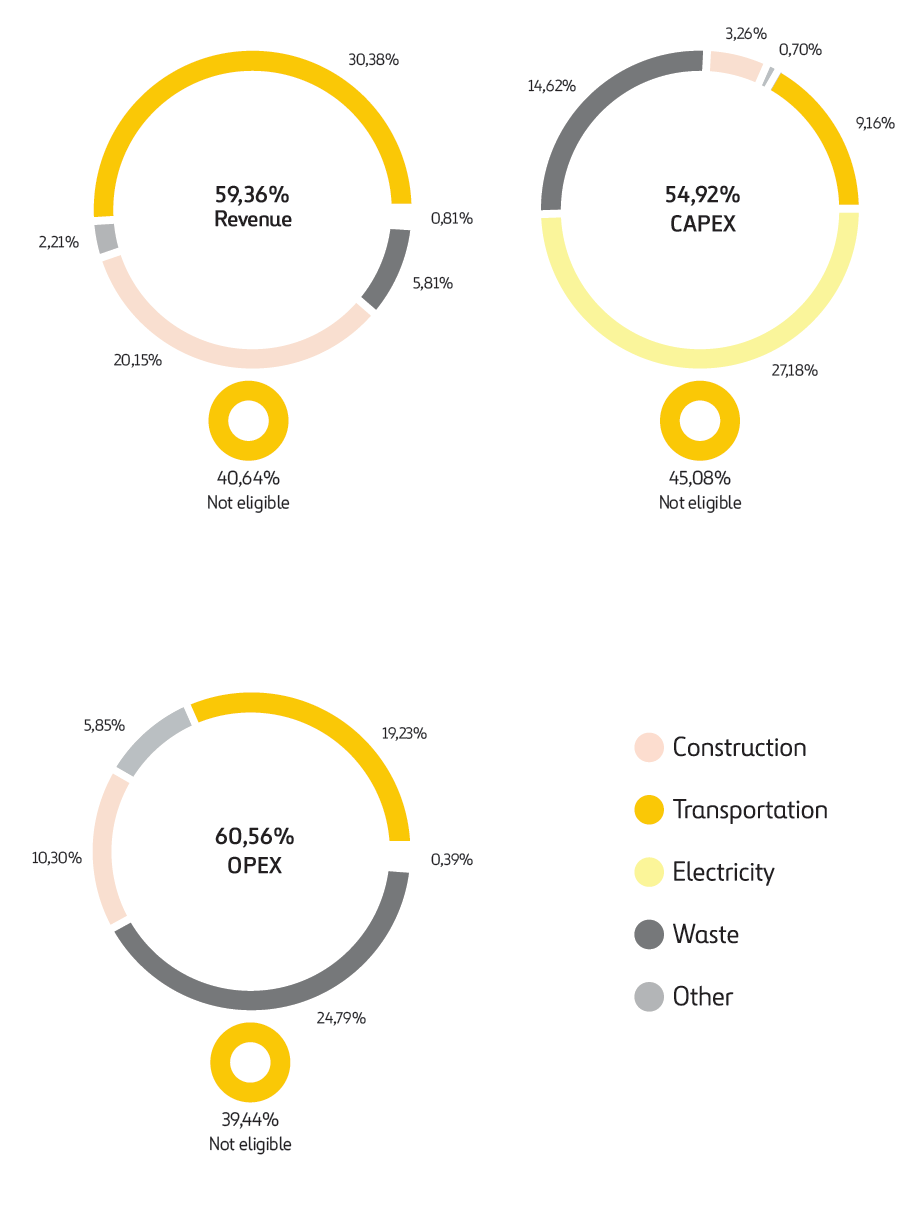

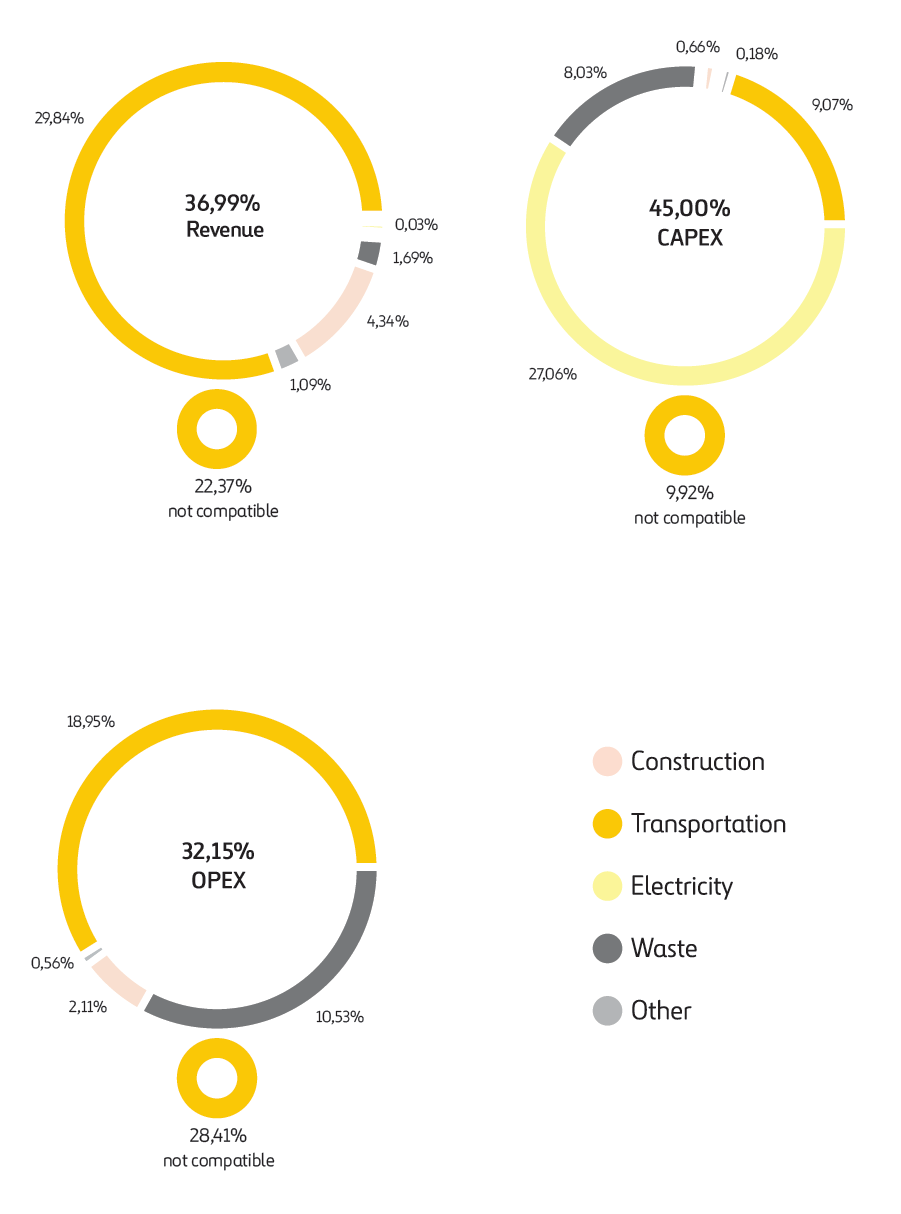

The results of the taxonomic analyses are shown in the graphical diagrams of figures: Taxonomy-eligible activities and Taxonomy-aligned activities.

Figure: Taxonomy-eligible activities

Figure: Taxonomy-aligned activities

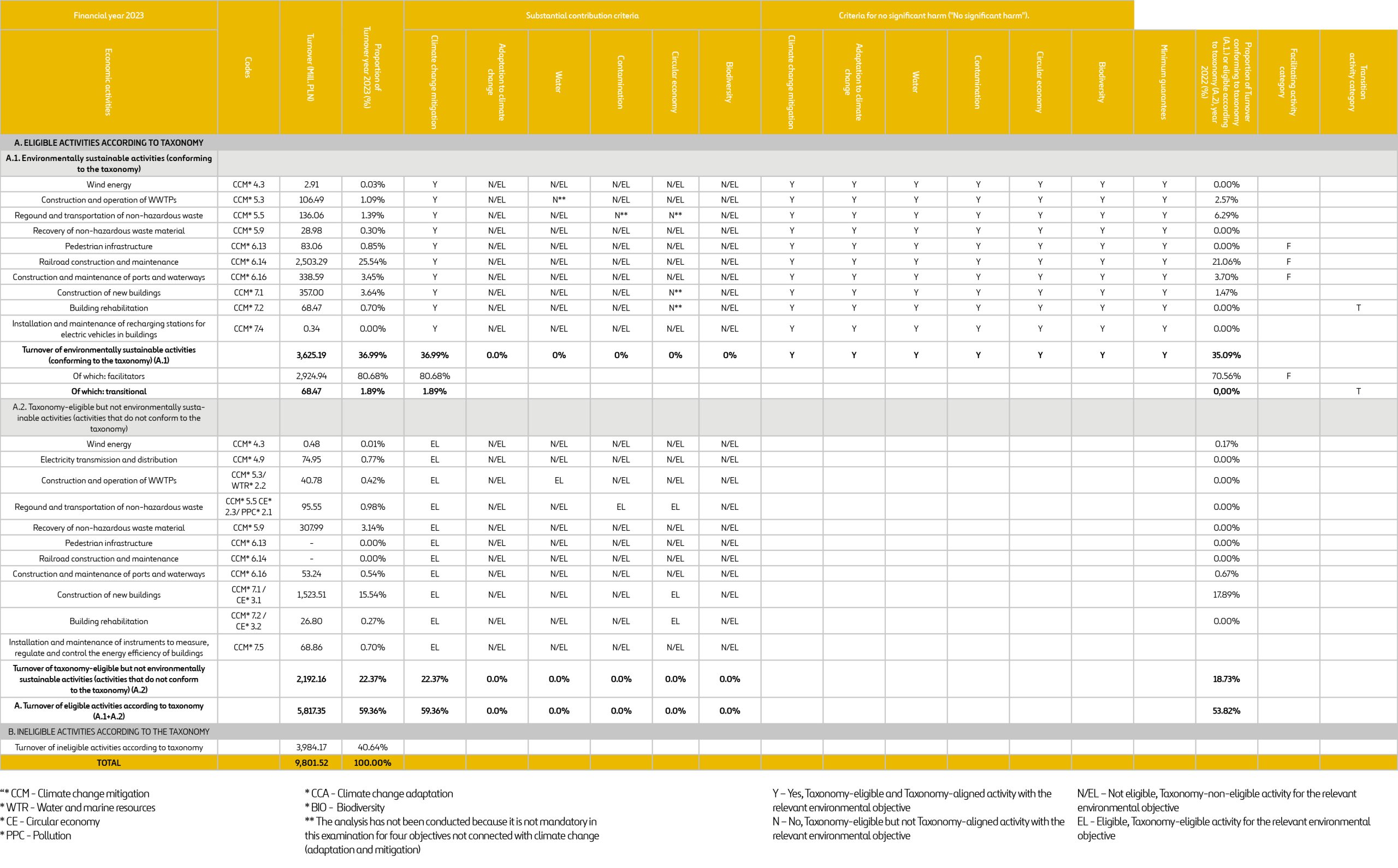

Table: Revenue

A full version of the table showing the revenue: HERE

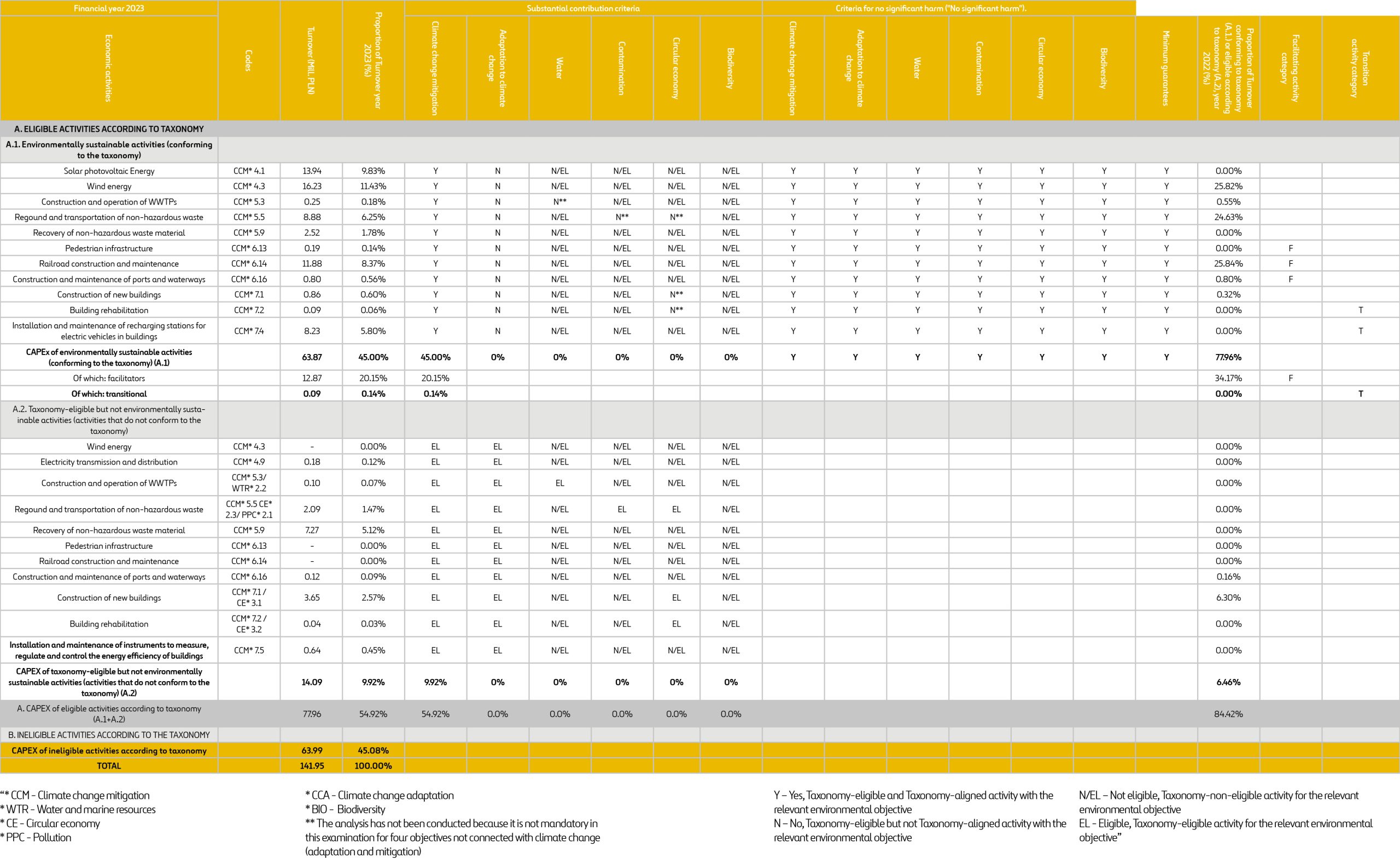

Table: CAPEX

A full version of the table showing CAPEX: HERE

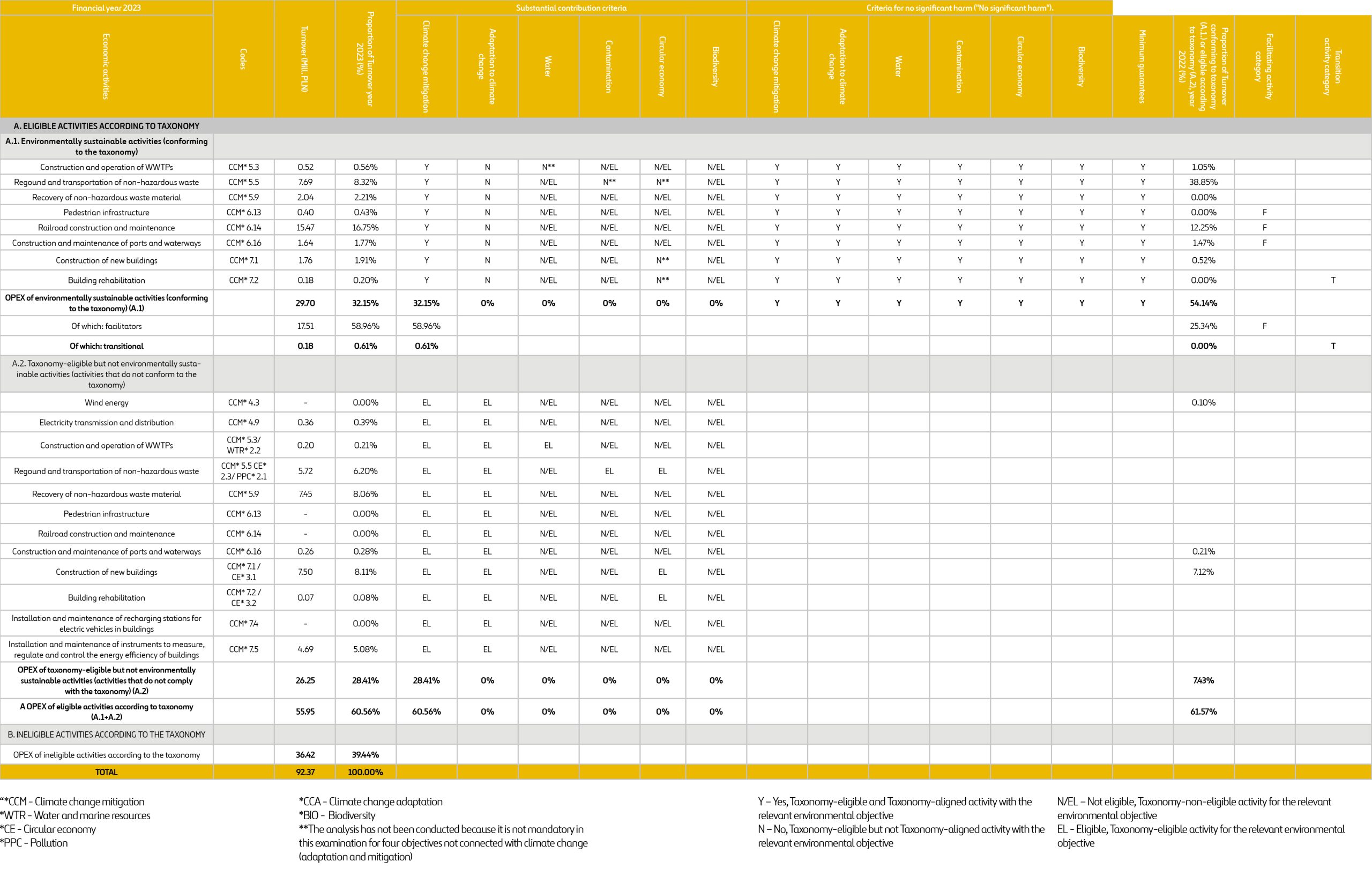

Table: OPEX

A full version of the table showing OPEX: HERE

The Group generates revenue from several business segments. most of which are included in the taxonomy in terms of Annexes I and II to the Delegated Climate Act (Commission Delegated Regulation (EU) 2021/2139).

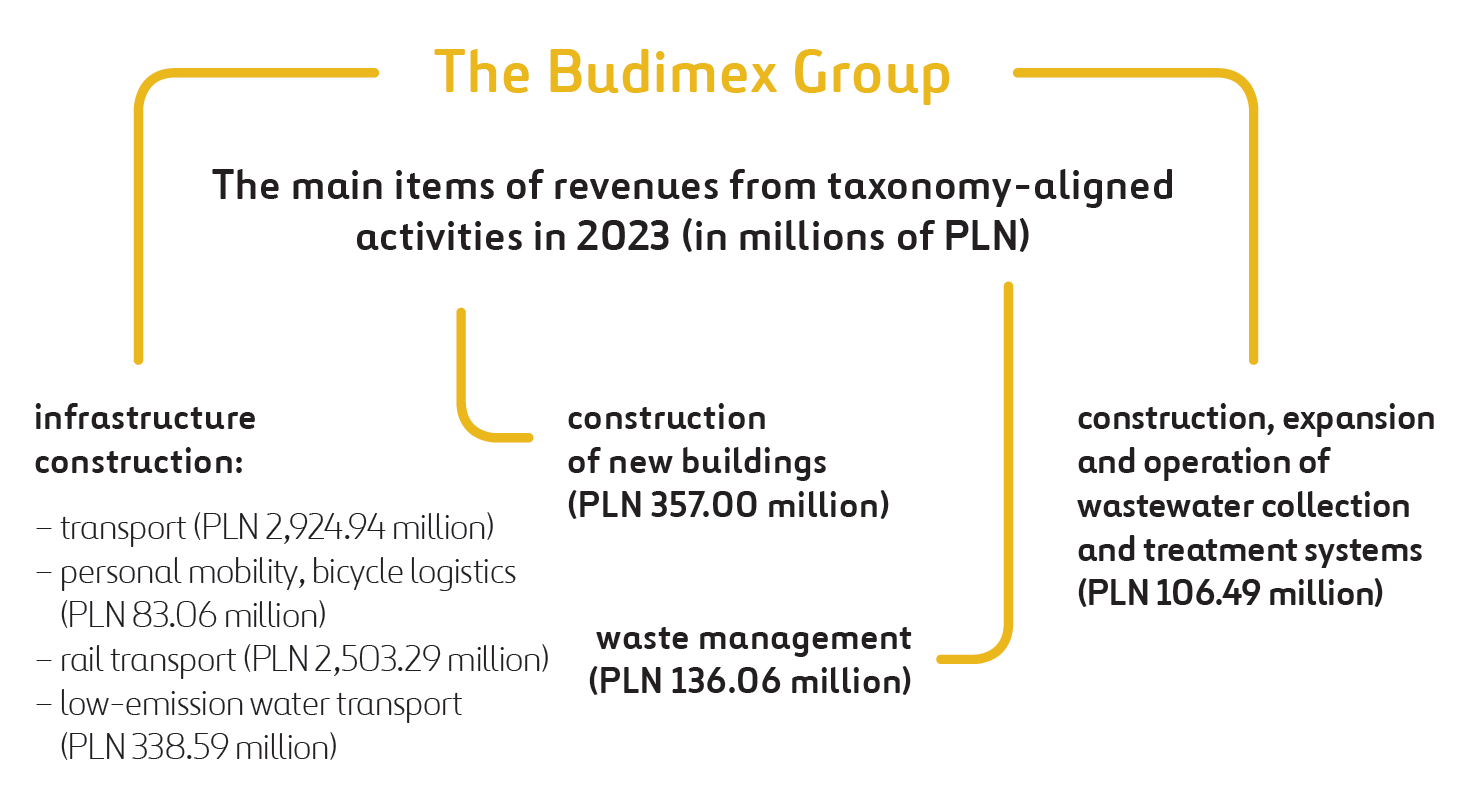

The main items of revenues from taxonomy-aligned activities in 2023 were:

- revenues from infrastructure construction contracts related to transport in the amount of PLN 2,924.94 million, related to the construction of infrastructure for personal mobility, bicycle logistics (PLN 83.06 million), the construction of infrastructure for rail transport (PLN 2,503.29 million) and infrastructure supporting low-emission water transport (PLN 338.59 million),

- revenues from the performance of contracts for the construction of new buildings in the amount of PLN 357.00 million,

- revenues related to the construction, expansion and operation of wastewater collection and treatment systems in the amount of PLN 106.49 million,

- revenues of the Group’s segment responsible for waste management amounted to PLN 136.06 million.

Some of the revenues generated relating to the aforementioned activities did not meet the technical eligibility criteria, and were therefore considered taxonomy-eligible but not aligned. This was particularly true of revenues from new building construction (PLN 1,523.51 million).

3,984.17 million in revenue came from taxonomy-non-eligible activities.

The share of taxonomy-eligible revenue in total revenue in 2023 was 59.36%, of which the share of taxonomy-aligned revenue of 36.99% and the share of taxonomy-eligible but not aligned revenue of 22.37%.

Capital expenditures (CAPEX) are related to the implementation of investment plans adopted by the Management Board. In 2023, taxonomy-aligned capital expenditures were primarily incurred for:

- construction of renewable energy production facilities, including wind energy (PLN 16.23 million) and using photovoltaic technology (PLN 13.94 million),

- waste management investments (PLN 8.88 million),

- installation, maintenance and repair of electric vehicle charging stations (PLN 8.23 million),

- other capital expenditures related to the types of activities from which construction taxonomy-aligned revenues were generated (PLN 16.59 million).

Part of the capital expenditures (PLN 14.09 million) were incurred in connection with construction activities relating to taxonomy-eligible but not aligned activities.

In addition, in 2023, the Group incurred capital expenditures of PLN 63.99 million related to taxonomy-non-eligible activities.

In 2023, the share of taxonomy-eligible capital expenditures in total capital expenditures was 54.92%, including the share of taxonomy-aligned capital expenditures – 45.00%, and the share of taxonomy-eligible but not-aligned capital expenditures – 9.92%.

Taxonomy-aligned operating expenses (OPEX) in 2023 amounted to PLN 29.70 million and were incurred to maintain in proper condition machinery, equipment, vehicles and other assets necessary for taxonomy-aligned activities. The largest item was related to the maintenance of assets necessary for the construction of infrastructure for rail transport (PLN 15.47 million).

In addition, in 2023, the Group incurred operating expenses of PLN 36.42 million related to taxonomy-non-eligible activities.

In 2023, the share of taxonomy-eligible operating expenses in total capital expenditures amounted to 60.56%, including the share of taxonomy-aligned operating expenses – 32.15%, and the share of taxonomy-eligible but not aligned operating expenses – 28.41%.

[1] Regulation (EU) 2020/852 of the European Parliament and of the Council of 18 June 2020 on the establishment of a framework to facilitate sustainable investment.

[2] Commission Delegated Regulation (EU) 2021/2178 of 6 July 2021 supplementing Regulation (EU) 2020/852 of the European Parliament and of the Council by specifying the content and presentation of information to be disclosed by undertakings subject to Articles 19a or 29a of Directive 2013/34/EU concerning environmentally sustainable economic activities, and specifying the methodology to comply with that disclosure obligation.

[3] NACE (French: Nomenclature statistique des Activités économiques dans la Communauté Européenne, Statistical classification of economic activities in the European Union) – a classification made up of a series of letters and numbers corresponding to five levels of classification.

[4] Until February 2024, Procurement, Quality and Environmental Protection Department.

[5] Commission Delegated Regulation (EU) 2021/2139 of 4 June 2021 supplementing Regulation (EU) 2020/852 of the European Parliament and of the Council by establishing the technical screening criteria for determining the conditions under which an economic activity qualifies as contributing substantially to climate change mitigation or climate change adaptation and for determining whether that economic activity causes no significant harm to any of the other environmental objectives.

[6] Commission Delegated Regulation (EU) 2022/1214 of 9 March 2022 amending Delegated Regulation (EU) 2021/2139 as regards economic activities in certain energy sectors and Delegated Regulation (EU) 2021/2178 as regards specific public disclosures for those economic activities.

[7] Until February 2024, Procurement, Quality and Environmental Protection Department.

[8] The Organisation for Economic Co-operation and Development.

[9] United Nations Guiding Principles.

[10] The database is available at: https://mneguidelines.oecd.org//database/.

[11] The database is available at: https://www.business-humanrights.org/en/companies.